Key Points Of The Article:

1.In 2019, the number of people experiencing hair loss in China exceeded 250 million, with an average of 1 in every 6 individuals affected. The group suffering from hair loss is trending younger, with 84% of people experiencing hair loss before the age of 30.

2.According to Moojing Analysis+, the sales revenue for anti-hair loss products on mainstream e-commerce platforms from December 2022 to November 2023 was 4.14 billion yuan, which is a decrease of 33.7% year-on-year. Additionally, regulations introduced in 2021 raised the development threshold for anti-hair loss products, leading to a general cooling of the market’s enthusiasm for this category.

3.Products like anti-hair loss essences and scalp treatments have grown against the trend. Professional care products are gradually becoming a part of consumers' daily routines. Moving forward, anti-hair loss products need to continuously upgrade along the path of specialized research and market segmentation.

National Health Commission survey data shows that as early as 2019, over 250 million people in China suffered from hair loss, or 1 in every 6 individuals. Among these, approximately 163 million were men and 88 million were women. The younger trend in hair loss is notable with 84% of sufferers experiencing hair loss before the age of 30, which is 20 years earlier than the previous generation. Nowadays, young people generally endure significant work-related stress. Long-term staying up late and poor dietary habits such as irregular and greasy food intake are common societal issues, which is why 'premature balding' is unsurprising.

Based on Moojing Social Listening, interaction volume on mainstream social media concerning the topic of anti-hair loss reached 150 million over the past year, which is a 172.6% increase year-on-year.

Although market demand continues to rise, sales revenue of anti-hair loss products on mainstream e-commerce platforms has been declining over the past year, and brands have slowed down the pace of new product development. This article will base its analysis on data from platforms such as Moojing Analysis+ and e-commerce listening, combined with publicly available market information to decode the development trends of anti-hair loss products, and identify concepts and categories that are growing against the trend.

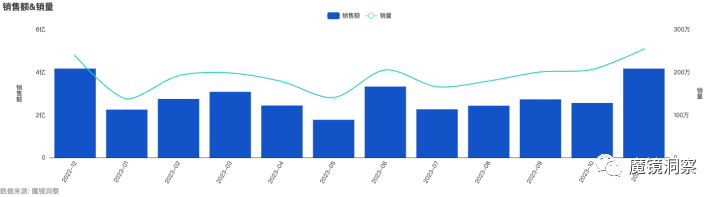

China's anti-hair loss market is large, with Guosheng Securities research reporting that the domestic hair growth industry is currently valued at approximately 114 billion yuan.According to Moojing Analysis+, sales revenue for anti-hair loss products on mainstream e-commerce platforms from December 2022 to November 2023 was 4.14 billion yuan, which dropped by 33.7% year-on-year, and the sales volume was about 29.845 million units, a decrease of 27.4%. This signifies a cooling in online sales.

The cooling of the anti-hair loss market is also reflected on the product side.

The "Cosmetics Supervision and Administration Regulation," enacted in 2021, posed new requirements for anti-hair loss products. Previously, regulatory agencies defined "hair fostering" as having three functions: promoting hair growth, preventing hair loss, and preventing hair breakage. After the enactment of the regulation, the concept of hair fostering will be gradually abolished. Most importantly, anti-hair loss products must pass human efficacy evaluations to prove they genuinely prevent hair loss in order to advertise this claim. The new regulations have further raised the threshold for anti-hair loss products. According to the National Medical Products Administration, as of 2023, only 63 anti-hair loss products are among the 5178 approved domestic special cosmetics.

At present, the market landscape of anti-hair loss products on e-commerce platforms is quite fragmented.The CR10 market share is about 37.7%, where old domestic brands and international giants move forward together. Due to the high barrier of entry, few new brands have entered the market. Domestic brands are mainly traditional ones such as Tongrentang and BaWang, centering their product concepts on traditional Chinese herbal components like ginger and Polygonum multiflorum; international brands include Foltène, renowned for its Western essential oil hair care, as well as the professional hair care brand Kérastase.

Moojing Analysis+ data shows that 76.7% of anti-hair loss products on e-commerce platforms are concentrated in the low-to-mid price range below 148 yuan, which is one of the main price segments chosen by consumers, accounting for about 35% of overall sales. The mid-to-high price range of 148-450 yuan is where consumers tend to purchase most, with sales making up over 50% of the total, but product quantity in this range is only about 20%, indicating a relative shortage in supply and opportunities for brands to focus on this segment.

Against the backdrop of the overall decline in anti-hair loss products, some concepts have grown against the trend.

Anti-hair loss essence is one of the better-performing categories within the market,according to Moojing Analysis+, between December 2022 to November 2023, the sales of this category on mainstream e-commerce platforms amounted to about 160 million yuan, an increase of 25% year-on-year, with sales exceeding 564,000 units.Anti-hair loss essence is known for its stronger efficacy and specificity. In recent years, it has become the choice of more and more "balding youths." According to Moojing Social Listening data, interactions related to anti-hair loss essence totalled 3.625 million over the past year.

In this niche market, the majority of the market share is occupied by international professional hair care brands like Foltène, Kangru, and Kérastase, with years of deep cultivation in the field of anti-hair loss and hair care, accumulating rich product development and marketing experience. In the top ten sales list, there are also some new brands with impressive growth. Next, we will screen brands and products that have sold over 1 million in the past year and have a year-on-year growth rate of over 100% for analysis.

The low price range below 276 yuan is a major purchasing choice for consumers, with nearly 80% of products in this segment, where market competition is fierce. The mid-to-high-end product line has significant development potential. FOLICULO密思丝密, a new brand focusing onPage 1 / 10 hair loss prevention and hair fostering, stands out in this high-end market.

FOLICULO密思丝密 is a scientist brand under Jieren, which launched its first product line at the end of 2021. The founder of the brand has held leadership positions in R&D at well-known international companies such as Procter & Gamble, Unilever, and General Motors, with a strong background in scientific research. Products under FOLICULO密思丝密 are priced between 439 to 3810 yuan, with the current best-selling product being a hair follicle nourishing ampoule for hair loss prevention, priced at 1280 yuan for 30 vials.

Official data shows that the product is jointly developed by scientists from China, the United States, and France, with a professional scientific endorsement. It includes proprietary ingredients such as hydrolyzed yeast protein and chicory root extract, as well as scalp care components, improving hair loss by reshaping the hair follicle growth environment.According to Moojing Analysis+, over the past year, this product achieved sales revenue exceeding 6.52 million yuan and ranked third in the scalp essence best-seller list during this year's Tmall Double 11 event.

Foltène belongs to the French pharmaceutical group Pierre Fabre and has a long history with global operations. According to Moojing Analysis+ data, its anti-hair loss essence products currently hold the number one market share of 25% on mainstream e-commerce platforms, with a 144.7% increase in sales revenue year-on-year.

The Triphasic Anti-Hair Loss Serum is a hit product from Foltène, and its sales over the past year have placed it at the top of the anti-hair loss essence rankings. The core ingredients of this product are Epilobium angustifolium extract and Cress extract, with a formula that boasts 40 years of R&D history. The product utilizes three "freshness-locking" technologies: powder, oil, and liquid are in separate states prior to use, mixed by the users themselves, and applied with an ergonomic massage head for scalp treatment, enhancing the overall user experience and engagement.

Additionally, Triphasic Anti-Hair Loss Serum also performs well in terms of repurchase rates. Moojing E-commerce Listening shows that 35% of the product-related comments involve repurchases.

YangYuanQing is a scalp care brand under Yunnan Baiyao, offering solutions for the scalp health of Chinese consumers with precious Chinese herbal materials. According to Moojing Analysis+ data, YangYuanQing stands out in the top 10 sales list for anti-hair loss essence on mainstream e-commerce platforms over the past year, being one of the few domestic brands and the only one with an average product price below 100 yuan.

Priced at 89 yuan, YangYuanQing's Anti-Hair Loss and Hair Fostering Liquid is remarkably "affordable" amongst the other anti-hair loss products that are priced in the hundreds or even thousands. This product also holds an invention patent. Its main components derive from natural plants and Chinese herbal medicines such as Platycladus orientalis leaves, Sophora flavescens, and Cnidium monnieri, purporting to create a healthy scalp environment. Currently,the cumulative sales revenue of YangYuanQing's Anti-Hair Loss Essence has reached 1.945 million yuan, a year-on-year growth rate of over 295%, and considering the light competition in a similar price range, the future growth potential is significant.

These three brands all hold invention patents and have efficacy validations from authoritative organizations in product R&D, but differ in product positioning. Whether it's Miss Secret, focusing on high-end ingredients, Yangyuanqing, priced affordably and specializing in traditional Chinese herbal formulations, or Furgreen Delight, with a long history and strong user experiences; each hit product stands firm in niche markets through distinct product features and solid product strength.

Against the backdrop of declining online sales of anti-hair loss products, the subcategory of "scalp care" still shows an upward trend. According to Moojing Market Intelligence+ data, from December 2022 to November 2023, the sales of anti-hair loss shampoo and conditioner products in this category reached nearly 600 million yuan, up 7.1% year on year.

A CBNData survey revealed that in 2023, over 80% of the population will specifically undertake scalp care, and the consumer awareness of "treating hair as you would skin" and the necessity of scalp care has increased significantly.

Through Moojing social listening, we found that within a rolling year, the volume of social media discourse on "scalp health" and "scalp care" increased by 311% sequentially, reaching 439,000 mentions, with interactions up to 68.24 million. Netizens even invented "early Vitamin C and evening Vitamin A" for hair care, and concepts such as scalp microbiome and anti-aging began to appear in hair and scalp care products.

Brands like Kérastase, Chando, and Off&Relax, both domestic and international, have since launched scalp care products with soothing, oil-controlling, antioxidative, strengthening barrier, balancing scalp flora, improving scalp micro-ecology, and anti-oxidation anti-aging effects. Taking Off&Relax as an example, its scalp repair serum achieved sales of 3.62 million yuan over a rolling year.

In summary, based on the development trends of anti-hair loss essences and scalp care products, professional-grade care products are gradually entering the daily lives of consumers. As the demographic of those experiencing hair loss expands and trends younger, Generation Z is becoming the main consumer force for anti-hair loss products. Furthermore, people's requirements for hair care ingredients and efficacy are increasing, and their purchase motivation is becoming more rational. In the face of market changes, brands need to use consumer data insights to understand demands. In the future, brands should continuously upgrade their products along the path of specialization and market segmentation, provide better solutions through scientific innovation in niche scenarios, thereby building core brand competitiveness.